Should you aggressively pay off your federal student loans, or consider Public Service Loan Forgiveness (PSLF)?

In this episode of the Finance For Physicians Podcast, Daniel Wrenne talks about different financial scenarios, opportunities, and strategies to avoid leaving money on the table when it comes to federal student loans.

Topics Discussed:

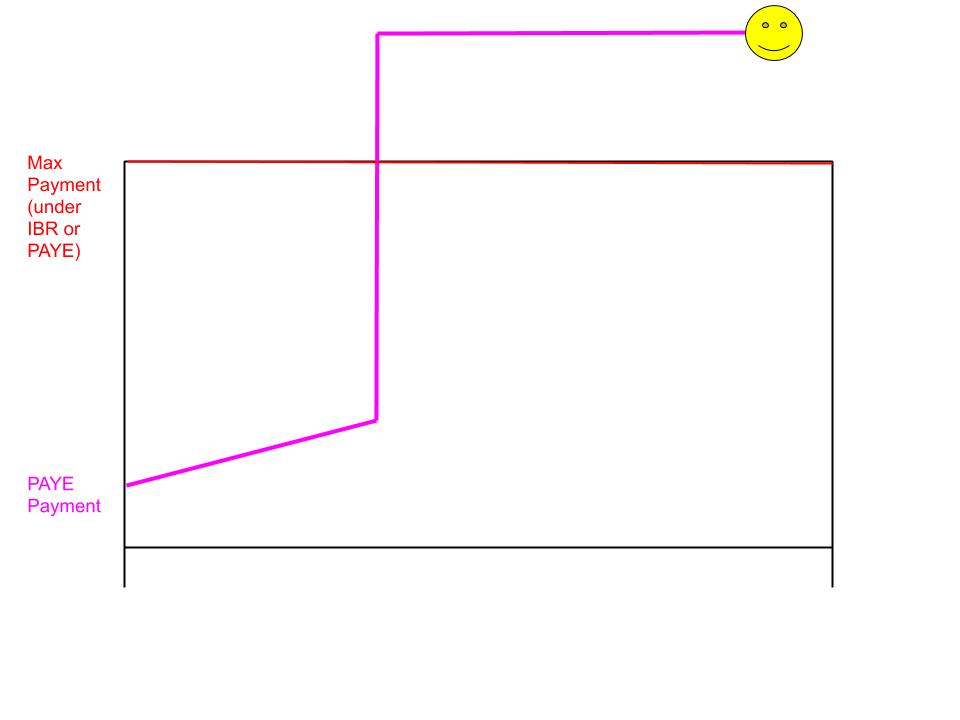

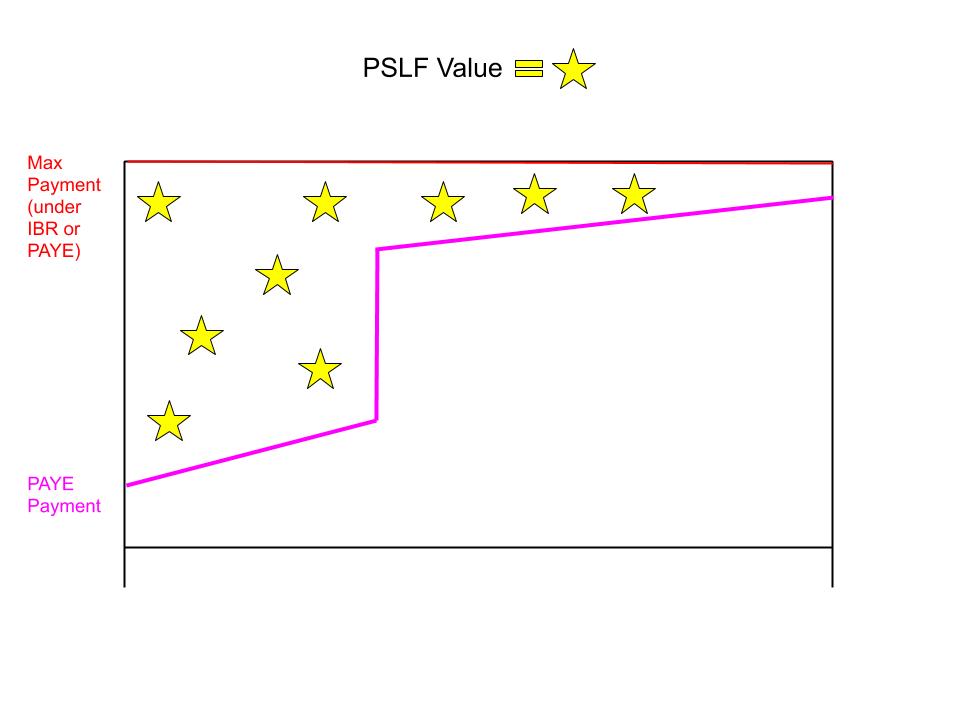

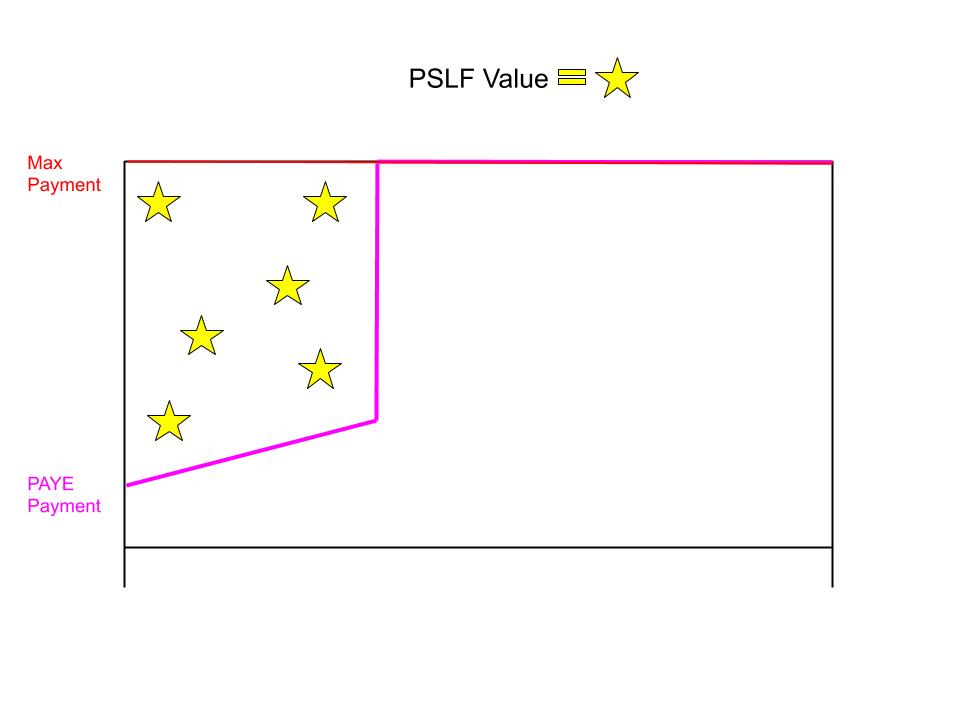

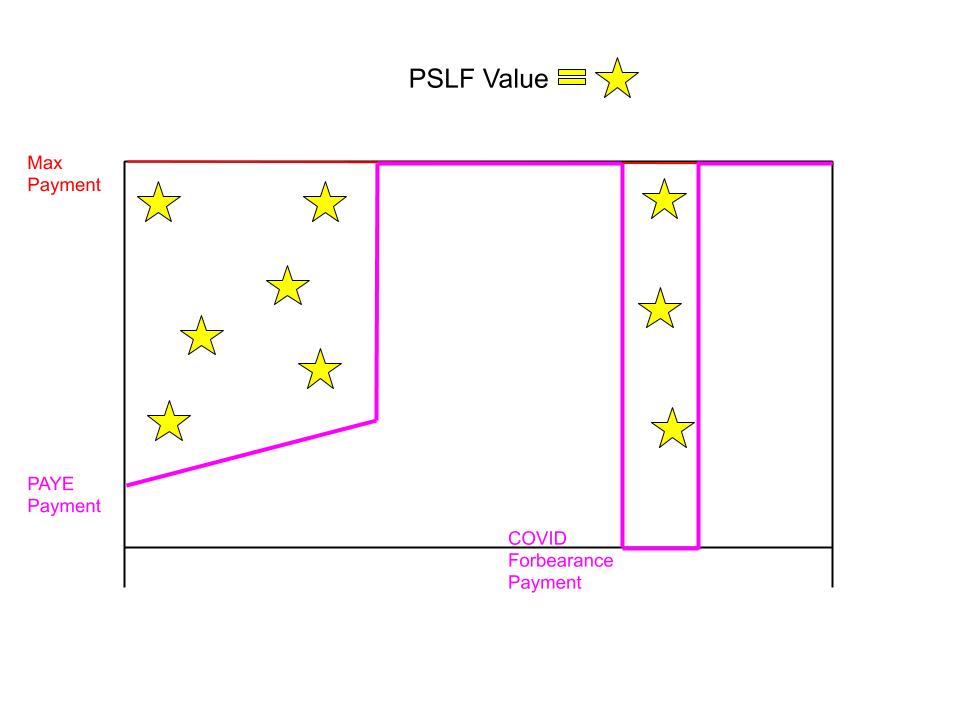

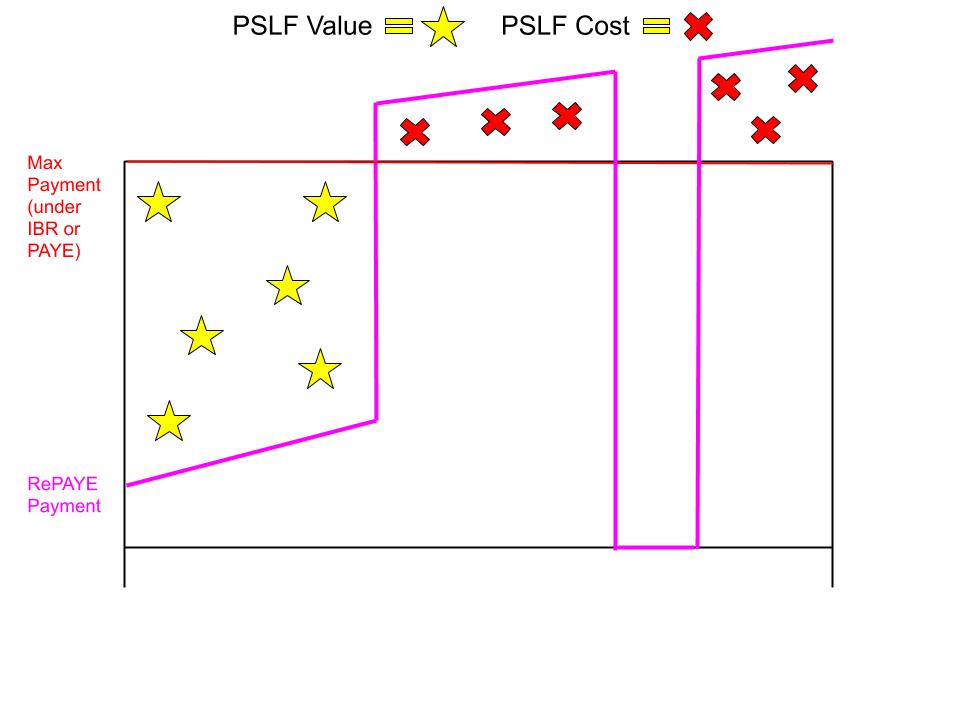

- Aggressive Payoff: Low payment in-training (under IBR or PAYE) + high payment in-practice = no PSLF value

- IBR/PAYE payment cap can lock in PSLF value even for physicians with ultra high in-practice income or with very low debt balances

- Verify current and future employer’s PSLF qualification status

- Normal PAYE Payments + PSLF: 120 PAYE payments under the payment ceiling = PSLF Value

- PSLF value originates from making qualified payments below the payment ceiling (less is more)

- Income driven repayment always lags actual return because it’s based on your most recent tax return AGI

- Payments Cap In-Practice + PSLF: PSLF value exists even when you hit the payment cap in-practice

- COVID Forbearance counts toward PSLF and adds huge value

- Strategies to reduce AGI and increase PSLF value

- RePAYE + Exceeding PAYE/IBR Payment Cap: Beware no payment cap

- In some cases, you can switch from RePAYE to IBR or PAYE (income must be under a certain threshold)

- FFEL and Perkins Loans do NOT qualify for PSLF (however, there are steps to work around this)

- Very payments by submitting employment certification (and always double check the math)

Links:

Public Service Loan Forgiveness (PSLF)

Federal Student Aid: Income-Driven Repayment Plans

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}